Insurance is designed to protect you from major, unexpected financial losses. But when damage occurs, many homeowners and drivers face the same question:

Quick Answer: If the damage is below or only slightly above your deductible, paying out of pocket may make more sense. If the loss is significant, involves liability, or would create financial hardship, filing a claim is often the better choice.

Should I file an insurance claim or pay for the repairs myself?

The answer depends on several factors:

- The size of the loss

- Your deductible

- Potential premium increases

- Future insurability concerns

- Whether liability is involved

Before filing a claim, it is important to understand both the immediate payout and the possible long-term impact on your insurance record.

Download Our Insurance Claim Decision Guide

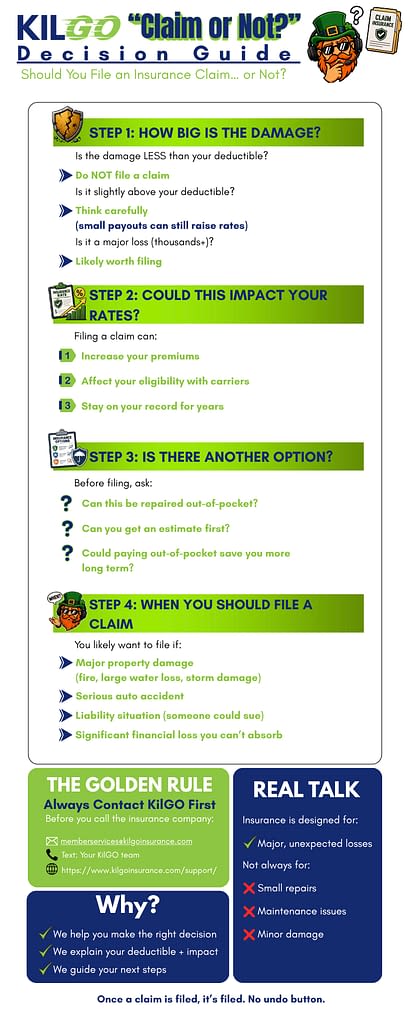

The First Question: How Much Damage Are We Talking About?

One of the easiest ways to evaluate a potential claim is to compare the repair cost to your deductible.

If the Damage is Less Than Your Deductible

In most situations, filing a claim does not make financial sense.

For example:

- $700 roof repair

- $1,000 deductile

The insurance company would typically pay nothing because the damage does not exceed your deductible.

If the Damage is Slightly Above Your Deductible

This is where many people make costly mistakes.

Consider:

- $1,500 repair bill

- $1,000 deductible

Your insurance company may only pay $500.

Before filing, ask yourself:

- Is a $500 payout worth a possible claims history entry?

- Could filing affect future premiums?

- Could it impact eligibility with preferred insurance carriers?

If the Damage is Significant

Insurance is generally intended for major losses such as:

- House fires

- Severe storm damage

- Major water losses

- Serious auto accidents

- Large liability claims

In these situations, filing a claim is often the appropriate choice.

Can Filing a Claim Affect Your Insurance Rates?

Many consumers are surprised to learn that filing a claim can have consequences beyond the current loss.

Potential impacts include:

- Higher future premiums

- Loss of claim-free discounts

- Changes in carrier eligibility

- Increased scrutiny at renewal

Every carrier evaluates claims differently, but your claims history often becomes part of your insurance record for several years.

Not Every Claim Raises Rates

It is important to understand that rate increases are not automatic.

Factors that may influence premium changes include:

- Claim type

- Claim amount

- Number of prior claims

- State regulations

- Carrier underwriting guidelines

For additional consumer guidance on claims, coverage, and insurance records, visit the National Association of Insurance Commissioners Consumer Resource Center.

Should You Get an Estimate Before Filing a Claim?

In many situations, yes.

Before contacting your insurance company, consider obtaining repair estimates from qualified contractors or repair facilities.

This helps you:

- Understand the actual cost of repairs

- Compare costs to your deductible

- Make an informed financial decision

- Avoid unnecessary claims reporting

Questions to Ask Before Filing

- Can I reasonably pay for this repair myself?

- Is the loss substantially greater than my deductible?

- Is there a possibility of future hidden damage?

- Could someone else be held liable?

- Would delaying reporting create problems?

When You Should Absolutely Consider Filing a Claim

There are situations where insurance is doing exactly what it was designed to do.

Major Property Damage

Examples include:

- Fire damage

- Large water losses

- Wind and hail damage

- Structural damage

Serious Auto Accidents

Examples include:

- Vehicle totals

- Injury accidents

- Multi-vehicle crashes

- Significant property damage

Liability Situations

If another person could potentially pursue legal action against you, it is usually wise to notify your insurer immediately.

Examples include:

- Slip and fall injuries

- Dog bite incidents

- Property damage to others

- Auto accidents involving injuries

Financial Losses You Cannot Comfortably Absorb

Insurance exists to protect your financial stability.

If a loss would create substantial hardship, filing a claim is often appropriate.

Common Claim Filing Mistakes Homeowners Make

Many claims that lead to frustration involve situations that insurance was never intended to cover.

Examples include:

- Deferred maintenance

- Wear and tear

- Gradual deterioration

- small cosmetic repairs

Insurance generally covers sudden and accidental losses, not ongoing maintenance issues.

For general consumer insurance information, visit the Consumer Financial Protection Bureau.

Frequently Asked Questions

Should I file a claim if the damage is only slightly above my deductible?

Not necessarily. If the insurance payout would be small, paying out of pocket may be the better financial decision.

Will filing a claim automatically increase my rates?

No. Rate impacts vary based on carrier guidelines, state regulations, claim type, and claims history.

How long does a claim stay on my insurance record?

Most claims remain visible for several years, though exact timeframes vary by insurer and reporting database.

Should I get repair estimates before filing?

In many cases, yes. Estimates help determine whether filing a claim is financially eneficial.

What types of claims should always be reported?

Serious accidents, liability situations, major property damage, and losses involving significant financial exposure.

The Golden Rule: Talk to Your Insurance Advisor First

Many policyholders assume they must immediately call the insurance company after discovering damage.

In reality, taking a few minutes to discuss the situation with your insurance advisor can help you make a more informed decision.

Before filing a claim, we can help you:

- Review your deductible

- Evaluate the size of the loss

- Discuss possible claim implications

- Understand your available options

- Determine appropriate next steps

Because once a claim is filed, it generally becomes part of your claims history.

Need Help Deciding Whether to File a Claim?

Not every loss requires an insurance claim.

If you’re unsure about your next step, contact our team before filing.

We help homeowners, drivers, motorcycle owners, RV owners, and landlords make informed insurance decisions every day.

Let us help you determine the best path forward.